If you’ve ever wondered which type of card impacts your credit history, you’re asking the right question. The cards you carry—and how you use them—can either strengthen your financial reputation or quietly damage it over time.

Your credit history plays a major role in loan approvals, interest rates, rental applications, and even job background checks in some cases. In this guide, we’ll break down which cards actually affect your credit, which ones don’t, and how to use the right card to build a strong credit profile.

Understanding Credit History: Why It Matters

Your credit history is a record of how you borrow and repay money. Lenders use this information to calculate your credit score, which reflects your reliability as a borrower.

Key factors that shape your credit history include:

-

Payment history (on-time vs. late payments)

-

Credit utilization (how much of your limit you use)

-

Length of credit history

-

Types of credit accounts

-

New credit applications

The type of card you use determines whether your activity gets reported to credit bureaus—and that’s what really matters.

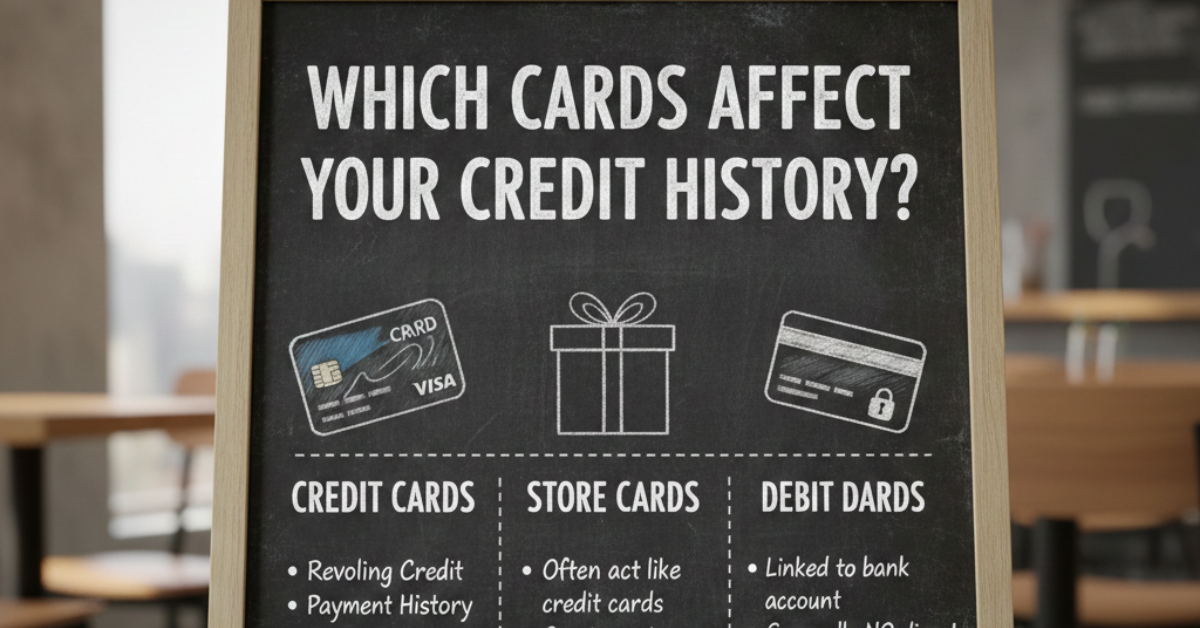

Which Type of Card Impacts Your Credit History?

1. Credit Cards (Biggest Impact)

Credit cards have the most direct and significant impact on your credit history.

When you use a credit card:

-

Your payment activity is reported monthly to credit bureaus

-

On-time payments improve your credit score

-

Late or missed payments hurt your score

-

High balances increase your credit utilization, which can lower your score

Best practices for building credit:

-

Pay your balance on time, every time

-

Keep utilization below 30% of your limit (under 10% is even better)

-

Avoid maxing out your card

-

Keep older accounts open to maintain credit history length

If you’re asking which type of card impacts your credit history the most, the answer is clear: traditional credit cards.

2. Store Credit Cards (Moderate to High Impact)

Retail or store cards function like regular credit cards but often come with:

-

Lower credit limits

-

Higher interest rates

-

Easier approval for beginners

They do impact your credit history because they report to credit bureaus. Used responsibly, they can help build credit. Misused, they can hurt quickly due to low limits and high utilization.

3. Secured Credit Cards (Great for Building Credit)

Why it matters:

-

Reports to credit bureaus just like a regular credit card

-

Ideal for people with no credit or poor credit

-

Helps establish positive payment history

For beginners or credit repair, this is one of the safest ways to positively impact your credit history.

4. Debit Cards (No Impact on Credit)

A debit card uses your own money from your bank account. Because you’re not borrowing:

-

Activity is not reported to credit bureaus

-

It does not build or affect credit history

-

Overdrafts generally don’t affect credit unless sent to collections

Debit cards are great for budgeting—but they won’t help your credit score.

5. Prepaid Cards (No Credit Impact)

Important points:

-

You load money in advance

-

No borrowing involved

-

No reporting to credit bureaus

-

No impact on your credit history

These cards are useful for spending control but won’t help you build credit.

Quick Comparison: Which Cards Affect Credit?

| Card Type | Impacts Credit History? | Best Use |

| Credit Card | Yes | Building and maintaining credit |

| Store Card | Yes | Entry-level credit building |

| Secured Card | Yes | Beginners or credit repair |

| Debit Card | No | Everyday spending and budgeting |

| Prepaid Card | No | Controlled spending without credit risk |

How Card Usage Affects Your Credit Score

Even with the right card, behavior matters more than the card itself.

Focus on these habits:

-

Pay on time (payment history = 35% of your score)

-

Keep balances low (credit utilization matters)

-

Avoid opening too many cards at once

-

Monitor your credit report regularly

The real answer to which type of card impacts your credit history is: any card that reports to credit bureaus—and your habits determine whether the impact is positive or negative.

FAQs

1. Do debit cards build credit?

No. Debit card transactions are not reported to credit bureaus, so they don’t affect your credit score.

2. Do prepaid cards help improve credit?

No. Prepaid cards do not involve borrowing and are not reported to credit agencies.

3. Which card is best for building credit from scratch?

A secured credit card is usually the best option for beginners or those with no credit history.

4. Can store cards hurt your credit?

Yes. High balances or missed payments can lower your credit score, especially because store cards often have low limits.

5. How fast can a credit card improve my credit?

With consistent on-time payments and low utilization, you may see improvement within 3–6 months.

Conclusion

So, which type of card impacts your credit history? The answer is simple: credit cards, store cards, and secured cards—because they report your activity to credit bureaus. Debit and prepaid cards, while useful for spending control, won’t help you build credit.

If your goal is a stronger credit profile, focus on one key strategy: use a credit-building card responsibly. Pay on time, keep balances low, and stay consistent. Over time, those small habits turn into a powerful financial advantage.